Key Takeaways

- Revolving credit offers businesses flexible access to funds up to a set limit.

- It supports cash flow management and can be reused without repeated approval.

- Mismanagement can lead to high interest costs and financial strain.

- Responsible usage and awareness of alternatives are essential for business health.

Understanding Revolving Credit

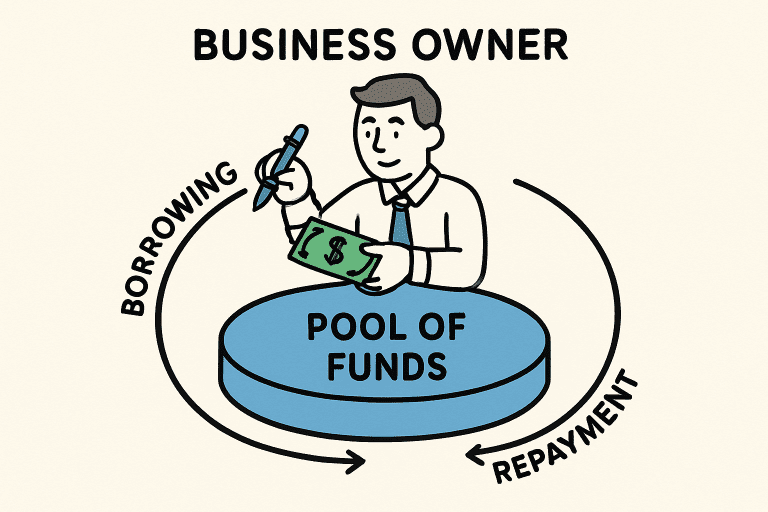

Revolving credit is a dynamic financial tool that empowers small businesses to draw funds up to a pre-approved limit, repay, and then use the funds again as operational needs arise. Unlike a traditional term loan, where you receive a one-time lump sum, revolving credit works more like a pool of money you can access repeatedly as long as you don’t exceed your maximum limit.

For businesses seeking reliable ways to manage cash flow fluctuations, SME credit facilities can serve as a flexible solution, providing ongoing access to funds without requiring reapplication each time a need arises. This structure is especially popular among small businesses with ongoing operational expenses or those that experience seasonal fluctuations in revenue.

The key difference between revolving credit and other forms of business lending is the freedom it offers: you pay interest only on the amount you’ve borrowed, not the entire credit line. This helps keep expenses lower and frees up capital for immediate and short-term business priorities.

Beyond mere convenience, revolving credit lines can be integral to a business’s resilience, enabling swift responses to unexpected expenses or opportunities that arise. Many lenders and banks offer this product specifically to suit the cash flow patterns of small and medium-sized enterprises.

Key Features of Revolving Credit

- Credit Limit: Every revolving credit facility comes with a cap set by the lender, which defines the maximum amount you can access at a given time.

- Flexible Repayments: Borrowers have the option to clear the balance in full or make minimum payments, with interest accruing only on the outstanding balance.

- Reusability: Once repayments are made, the facility resets, letting businesses access their full credit line as often as needed, within agreed-upon terms.

Benefits for Small Businesses

The real value of revolving credit for small businesses lies in its unparalleled flexibility and convenience:

- Cash Flow Management: Revolving credit enables businesses to maintain stability during seasonal slowdowns, unexpected expenses, or gaps in accounts receivable, ensuring they can consistently cover payroll and bills when revenues fluctuate.

- Operational Agility: Funds can be drawn down for varied uses—from emergency equipment repairs to taking advantage of vendor discounts through early payments—making revolving lines adaptable for almost any business need.

- Interest Efficiency: With revolving credit, companies pay interest only on the portion drawn, not the full approved amount. This structure can significantly lower borrowing costs compared to term-based options.

According to the Inc. Guide to Credit Options, many small enterprises rely on lines of credit as an ‘insurance policy’ against uncertainty, preserving their growth trajectory despite bumps in the road.

Potential Drawbacks

While the advantages are significant, there are important risks and limitations to consider with revolving credit:

- Higher Interest Rates: Revolving facilities often carry higher interest rates compared to conventional term loans, particularly when the outstanding balance remains high over time.

- Debt Cycle Risk: Easy access to funds can tempt businesses to overuse their available credit, potentially leading to a debt spiral that’s difficult to escape.

- Variable Interest Rates: Many revolving credit products feature adjustable rates, meaning monthly payments can increase unexpectedly, complicating budgeting.

Impact on Financial Health

Recent research by J.D. Power highlights a critical challenge: over half of small businesses are deemed financially unhealthy, with 61% of these carrying ongoing revolving debt through credit cards. Without careful monitoring and repayment discipline, the flexibility of revolving credit can quickly become a liability.

Strong financial health hinges on not just access to funds, but on prudent borrowing and regular review of how these products are used within your business’s capital structure.

Best Practices for Managing Revolving Credit

To derive the most value from revolving credit—while minimizing risks—small businesses should implement these proven practices:

- Monitor Credit Utilization: Consistently keep your credit utilization ratio under 30%—this not only protects your credit score but ensures borrowing doesn’t outpace repayment capacity.

- Make Timely Payments: Always make at least the minimum payment by each due date. Late or missed payments often result in penalty fees and higher future interest rates.

- Periodic Review: Review your business’s need for a credit line every quarter. Adjust your limit as the business grows, or restrict access during leaner cycles.

Alternatives to Revolving Credit

While revolving credit is often effective for daily operations and short-term needs, there are other products better suited to long-term investments or specific financing challenges:

- Term Loans: Structured borrowing for larger, pre-defined investments, such as new equipment or office expansion. Repayment is in set amounts over a specified period.

- Invoice Financing: Unlocks cash tied up in receivables by borrowing against your unpaid invoices—ideal for companies whose clients have extended payment terms.

- Merchant Cash Advances: Offer upfront funding in exchange for a percentage of ongoing credit card sales, although often at higher total costs and fees.

Each alternative has advantages and trade-offs. Evaluate your business’s financing needs, risk tolerance, and repayment capacity to select the right product mix.

Final Thoughts

Revolving credit stands out as a powerful, flexible option for small businesses, enabling agility and resilience in a constantly changing business environment. With careful management, a clear understanding of its features, and strategic selection of complementary financing solutions, small businesses can leverage revolving credit to support growth, stability, and long-term success.